This article was originally written by Nicholas Rossolillo of The Motley Fool.

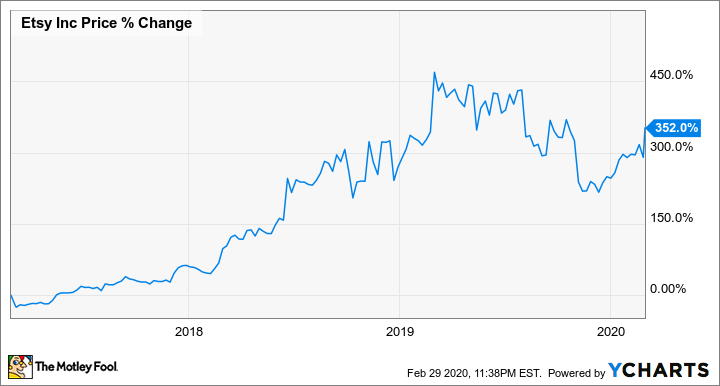

Up until last year, Etsy (NASDAQ:ETSY) was one of those hot stocks I'd been watching for years but stayed away from. The e-commerce platform for crafts and handmade goods is up over 350% over the last three years. 2019 was a rough patch for the stock, though, and after watching it retrace a good portion of its gains as investors reset future expectations, I decided to finally pull the trigger at the beginning of the new year.

I'm glad I did, and shares still look like a reasonable value to me given the 2020 outlook. With the tailwinds moving the e-commerce industry forward still gusting, Etsy stock remains a buy in my book.

DATA BY YCHARTS.

A recap on another great year

When CEO Josh Silverman took the reins at Etsy in 2017, his aim was to simplify the company by focusing on "the fewest things that can make the greatest impact for buyers and sellers." Over the summer of 2018, that meant an increase in the fee charged to sellers (at 5%, it's still far less than the competition), so the company could invest in improving the user experience (like free shipping for shoppers and Etsy ads for sellers), migrate its back-office operations to the cloud, and launch new advertising to drive traffic to the site (like its holiday 2019 TV campaign).

As a result of the changes, Silverman and the top team laid out a plan in the spring of 2019 to increase gross merchandise value sold on its platform by 16% to 20% each year for the next five years, and for revenue to outpace that amount each year. So far so good. The value of goods sold grew by 20% in 2019 (excluding the addition of the Reverb online music equipment site).

| Metric | Full-Year 2019 | Full-Year 2018 | Change |

|---|---|---|---|

| Revenue | $818 million | $604 million | 36% |

| Operating expenses | $459 million | $338 million | 36% |

| Earnings per share | $0.76 | $0.61 | 25% |

| Adjusted EBITDA | $186 million | $140 million | 34% |

DATA SOURCE: ETSY. EBITDA = EARNINGS BEFORE INTEREST, TAX, DEPRECIATION, AND AMORTIZATION.

Also of note are Etsy's high profit margins, especially given that it's a company in growth mode. Silverman mentioned the nearly 23% adjusted EBITDA-to-revenue margin on the earnings call and cited the rule of 40 -- a metric used by some investors in high-growth companies with thin profit margins. If a stock's revenue growth rate plus its profit margin (or minus, if profit margin is negative for a company operating at a loss) exceeds 40, it's a buy. With a score of 59 in 2019 -- 36% revenue growth plus 23% EBITDA-to-revenue margin -- Etsy is a buy.

A reasonable valuation if you believe there's fuel in the tank

For a more traditional take on the stock, though, let's use free cash flow (what's left after cash operating and capital expenses are paid). Based on the $190 million of free cash Etsy generated last year, shares currently trade for 36 times profits. Not cheap but reasonable given the growth management is targeting.

And on that front, 2020 is looking to deliver once again. Gross merchandise value is expected to grow 25% to 28% and revenue by 27% to 30% (which would mean $1 billion in annual sales for the first time). Management is also guiding for adjusted EBITDA margin between 21% and 22%. Shares currently trade for 30 times adjusted EBITDA at the midpoint of guidance (based on an outlook of $220 million to $235 million).

Put simply, Etsy looks like a real value if it can keep up its current pace of expansion. It isn't the perfect stock for everyone, as it will likely continue to be a volatile ride given the premium valuation. But for those in it for the long-term potential that management has outlined, this e-commerce company is a buy.

MyWallSt operates a full disclosure policy. MyWallSt staff currently hold no positions in Uber. Read our full disclosure policy here.

Nicholas Rossolillo owns shares of Etsy. The Motley Fool owns shares of and recommends Etsy. The Motley Fool has a disclosure policy.

- New stock picked every week out of 60,000 worldwide

- Ten Foundational stocks to hold until 2034

- A library of 60 stocks with analysis

- 10 year Track record of performance