Should You Buy or Sell Airline Stocks Right Now?

Join thousands of savvy investors and get:

- Weekly Stock Picks: Handpicked from 60,000 global options.

- Ten Must-Have Stocks: Essential picks to hold until 2034.

- Exclusive Stock Library: In-depth analysis of 60 top stocks.

- Proven Success: 10-year track record of outperforming the market.

This article was originally written by Lou Whiteman of The Motley Fool

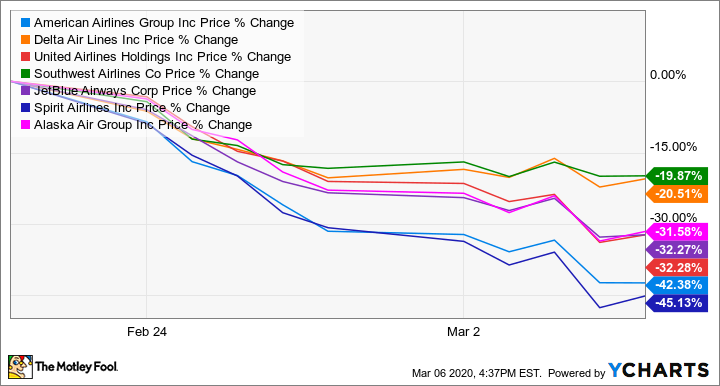

Airline shares have been decimated by the COVID-19 coronavirus sell-off, with some stocks losing nearly half of their value in the last two weeks alone. And not without reason.

As the coronavirus has spread globally, travel demand has plummeted, with United Airlines Holdings (NASDAQ:UAL) saying it saw near-term demand to all of Asia fall by more than 75% when the virus was largely contained to China. The airlines have canceled flights to parts of the world that have been heavily affected, and some, including United and JetBlue Airways (NASDAQ:JBLU), have announced plans to scale back service across their entire networks until demand resumes.

AIRLINE STOCKS YEAR TO DATE DATA BY YCHARTS

The airline sector has long been highly cyclical, and the downturns have usually been painful for investors. Storied names like Eastern Airlines, TWA, Braniff, and PanAm disappeared from the skies during past downturns.

Nothing is certain about the ultimate effects coronavirus will have on the economy at large, and airlines in particular, but it does appear the blow will be substantial. It's a scary time to be holding airline shares. But for those with a long time horizon, and the stomach to handle turbulence, here's why it's a great time to buy.

This is material, but not permanent

Wall Street tends to be focused on quarterly results, and there is little doubt the coronavirus will affect airline financials at least for the first half of 2020. That could extend into the second half of the year as well. During a TV appearance, Southwest Airlines (NYSE:LUV) CEO Gary Kelly said the drop in demand is reminiscent of what happened after the attacks on Sept. 11, 2001.

In years past that might have been enough to permanently ground a U.S. airline, and based on the stock reactions in recent weeks, memories of past crises are weighing heavily on investors this time around. However, the industry has changed dramatically.

A period of restructuring and consolidation in the early 2000s reduced the number of airlines competing for business and fortified the balance sheets of the survivors. Today Delta Air Lines (NYSE:DAL), American Airlines Group (NASDAQ:AAL), United, and Southwest control about 80% of the U.S. market, giving them unprecedented pricing power.

The coronavirus could cause changes in behavior, for example, boosting teleconferencing over business travel. There is also the risk the virus-related slowdown could lead to a U.S. recession that could soften corporate travel demand. But there is nothing to suggest there will not be an eventual recovery. If past virus outbreaks are a guide, tourism and leisure travel will return first, possibly as soon as this summer, because it is more easily stimulated by fare sales.

Prior to coronavirus, the International Air Transport Association had projected that global air traffic will double over the next two decades. Near-term earnings are likely to tumble because of the outbreak, but in all likelihood the long-term growth forecast will not be altered. And fortunately for investors, all major airlines have the balance sheets to weather a near-term disruption.

Airlines are healthier than they have ever been

In past downturns airlines failed because the industry has massive fixed costs tied to airplane purchases, and with so many competitors chasing a limited number of fliers, pricing discipline went out the window. Consolidation has helped on the pricing side, and the post-9/11 bankruptcies of Delta, American, and United have helped bring costs under control as well.

American's share price fall has been the most dramatic among major airlines because the company has $24 billion in long-term debt, the most in the industry, and is therefore seen as the most vulnerable to a prolonged downturn. The company went into 2020 hoping to use profits to pay down that debt total by as much as $4 billion over the next two years, and coronavirus has certainly cast doubt on that plan.

But American and its peers are far from a cash crunch. The company successfully raised more than $1 billion earlier in the year and has significant unencumbered assets to borrow against if it needs more cash in a pinch. At year's end, it also had about $7.1 billion in total available liquidity under its borrowing agreements.

Spirit Airlines (NYSE:SAVE) has fallen nearly as much as American, which is perhaps unsurprising given that the company's 31% debt to asset ratio is the only U.S. airline approaching American's 40% figure. The company's shares have also been beaten down because it was expected to be one of the fastest-growing airlines in 2020, and its valuation prior to the outbreak reflected an outlook for growth that now seems unlikely to materialize. But Spirit, like American, is not cash constrained, with more than $1 billion in cash at year's end.

The industry also has the support of Washington, with the White House reportedly willing to consider deferring taxes to help stem the economic fallout of the slowdown. The bottom line is that every publicly traded U.S. airline has considerable runway ahead of it before the coronavirus becomes a severe financial crisis.

Warren Buffett, who famously said investors should be greedy when others are fearful, manages a basket of airline stocks inside Berkshire Hathaway. We won't know for sure what Buffett was buying and selling as markets turned south until quarter-end disclosures, but we do know Berkshire added to its massive Delta stake in late February.

Buy for the long haul

Investors looking at the airline sector need to understand this could get worse before it gets better. The global industry has lost more than $40 billion in combined market capitalization in February alone, about one-fifth of its total, according to British investment firm AJ Bell. That sort of drop is driven by emotion, and not financials, and until the full extent of the coronavirus is known it could be hard for airline stocks to find a bottom.

That said, the long-term outlook for the industry is not 20% worse today than it was in early January. Investors willing to buy in today and ride through the headwinds have the opportunity to buy quality operators like Delta at six times earnings, less than half the multiple investors were paying for the stock a little more than a year ago.

Be careful bargain hunting: Companies like American and Spirit have fallen the most because their upside is delayed more than most due to coronavirus and could be facing multi-year recoveries. But for those who can ignore the headlines, keep a focus on the long term, and be selective about what they buy, it is an intriguing time to buy airline stocks.

MyWallSt operates a full disclosure policy. MyWallSt staff currently hold long positions in companies mentioned above. Read our full disclosure policy here.

Lou Whiteman owns shares of Berkshire Hathaway (B shares), Delta Air Lines, and Spirit Airlines. The Motley Fool owns shares of and recommends Berkshire Hathaway (B shares), Delta Air Lines, Southwest Airlines, and Spirit Airlines. The Motley Fool recommends JetBlue Airways and recommends the following options: long January 2021 $200 calls on Berkshire Hathaway (B shares), short January 2021 $200 puts on Berkshire Hathaway (B shares), and short March 2020 $225 calls on Berkshire Hathaway (B shares). The Motley Fool has a disclosure policy.

- Weekly Stock Picks: Handpicked from 60,000 global options.

- Ten Must-Have Stocks: Essential picks to hold until 2034.

- Exclusive Stock Library: In-depth analysis of 60 top stocks.

- Proven Success: 10-year track record of outperforming the market.