Tesla: How Much Is Hype and How Much Is Real?

Join thousands of savvy investors and get:

- Weekly Stock Picks: Handpicked from 60,000 global options.

- Ten Must-Have Stocks: Essential picks to hold until 2034.

- Exclusive Stock Library: In-depth analysis of 60 top stocks.

- Proven Success: 10-year track record of outperforming the market.

This article was originally written by Pavan Gadiraju of The Motley Fool.

One undeniable fact about Tesla (NASDAQ:TSLA), acknowledged by even the company's detractors, is that it practically invented the electric vehicles (EV) market. Experts who dismissed Tesla founder Elon Musk's initial pronouncements about the demand for a mass-produced electric car as just hype had to eat their words as the company established a whole new market.

Any other company in Tesla's place would have worked to capitalize on its initial success by making and selling as many cars as possible, fully leveraging its first-mover advantage. But Tesla investors have been waiting for that to happen for years, and every time it seems the company is getting its act together, bulls have flocked to the stock only to find themselves wrong footed one more time. Shares have been rallying again over the past several months, and that begs the question -- Will Tesla finally live up to its hype?

The $4,000 prediction

Since Tesla reported its third-quarter results on Oct. 23, the stock has surged 40% to nearly $360 per share. Soon after that report, one of Tesla's biggest bulls, Catherine Wood of Ark Investment Management, reaffirmed the case for the stock's eventual rise to $4,000 per share -- and beyond. Wood made the case earlier this year for this jaw-dropping valuation based on two major assumptions: 1) the emergence of a Tesla autonomous ride-hailing network, and 2) a prediction that Tesla would be selling more than 1.5 million electric vehicles annually by 2023.

Both Ark and Elon Musk have said some really fanciful things regarding that first assumption. Based on one Ark analyst's argument on how far ahead Tesla is in fine-tuning its self-driving algorithm, thanks to the data being generated by Tesla vehicles currently on the roads, she sees a fleet of Tesla robo-taxis generating income for its owners in the near future. Musk himself has touted this idea by suggesting that, when the potential future income generated by self-driving Tesla taxis is accounted for, the present value of a Tesla is far higher than the ticket price an owner pays, and that "It will be financially insane to buy anything other than a Tesla."

But if Tesla is to live up to its mega-valuation, the second assumption from Ark's model is also important -- the road to 1.5 million-plus vehicles per year. That could be the foundation Tesla needs to capture the burgeoning global market for EVs.

China's shadow looms large once again

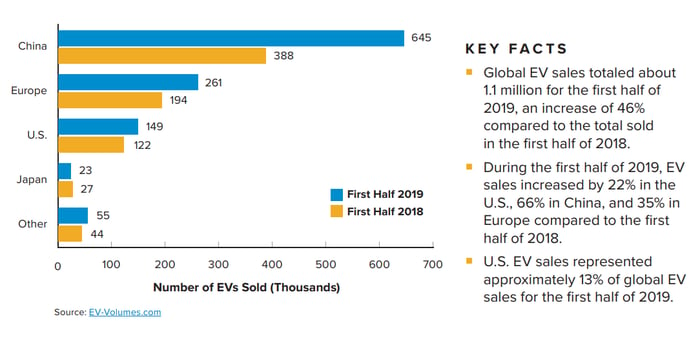

The chart below compares global EV sales from the first half of 2018 and 2019.

IMAGE SOURCE: EDISON ELECTRIC INSTITUTE

And what's the obvious inference from the chart above? China continues to be the fastest-growing market for EVs with sales up 66% year over year in the first half of 2019. And that fact is not lost on Elon Musk. Tesla's efforts to accelerate its schedule for the Gigafactory in Shanghai is a testimony to this.

Even then, by the company's own statements, its initial goal is to make 250,000 cars a year in its Shanghai factory before ramping up the production to 500,000 units. With no indication of the timeline for these numbers to come to fruition, and given the history of Tesla coming up short on its big promises, Tesla is far away from the reality of building "more than 1.5 million vehicles" in just four years' time.

Besides hitting its own production targets, Tesla's competitors are lining up, and the company will have a lot of catching up to do with China's own EV makers. One such example, Nio, is offering the ES8 SUV to give Tesla's Model X a run for its money with comparable specs and a lower price tag. With China accounting for 56% of global EV sales in 2018, Nio and its peers are a thorn in Tesla's side, but for now, they're available only in China. If and when these new EVs are made available in Europe (where Tesla is arguably the only EV player at the moment) and in broader Asia, Tesla might have a tough time fighting the low-cost competitors.

Closer to home, traditional automakers from the U.S. and Europe are also upping the ante with their own EV offerings. They're working to close the gap with Tesla in terms of performance, and perhaps more importantly, they're also working toward closing the gap with Tesla in terms of desirability, as showcased by Ford's latest EV offering with the iconic Mustang branding, creating a buzz among both traditional car enthusiasts and the tech-minded.

Hype vs. reality

When friends ask me for my opinion on the $4,000 prediction for Tesla stock, I tell them this: If the stock doubles in price from its present level, already within reach of the stock's all-time high, to about $800 per share, I'll buy and hold it for a long time.

But with all of this incoming competition and the EV market quickly transforming into one where consumers will have the level of choice they do with every other purchase, Tesla's most bullish supporters seem to need a reality check as they consider the future of the company. Tesla invented the EV market and is an exciting company to follow, but that "hype" does not replace the critical eye every investor should have as they evaluate a company, especially a high-growth one with a wide-eyed fan base both in and out of the market.

MyWallSt operates a full disclosure policy. MyWallSt staff currently hold long positions in companies mentioned above. Read our full disclosure policy here.

Pavan Gadiraju has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Tesla. The Motley Fool has a disclosure policy.

- Weekly Stock Picks: Handpicked from 60,000 global options.

- Ten Must-Have Stocks: Essential picks to hold until 2034.

- Exclusive Stock Library: In-depth analysis of 60 top stocks.

- Proven Success: 10-year track record of outperforming the market.